快速开始

交易任务

从零开始构建一个交易任务

1. 根据目录结构创建文件

源码目录结构:

kfx-task-condition-demo/ # 交易任务文件名(英文名称,随意)

├── src/

│ └── python

| └── ConditionOrder # 交易任务名称(英文名称,随意)

| └── __init__.py # python交易任务策略代码

├── README.md # 交易任务说明

└── package.json # 编译配置信息

交易任务实现代码 __init__.py

1import kungfu

2from kungfu.wingchun.constants import *

3import json

4import time

5import math

6import threading

7from datetime import datetime

8from pykungfu import wingchun as wc

9

10yjj = kungfu.__binding__.yijinjing

11

12

13class Config(object):

14 def __init__(self, param):

15 sourceAccountList = param["accountId"].split("_")

16 self.marketSource = param["marketSource"]

17 exchangeTicker = param["ticker"].split("_")

18 self.side = Side(param["side"])

19 self.offset = Offset(param["offset"])

20 self.priceType = PriceType(param["priceType"])

21 self.volume = int(param["volume"])

22 self.maxLot = int(param.get("maxLot", 0))

23 self.startTime = str_to_nanotime(param.get("startTime", "0"))

24 self.orderPrice = param["orderPrice"]

25 self.source = ""

26 if len(sourceAccountList) == 2 and len(exchangeTicker) == 5:

27 self.source = sourceAccountList[0]

28 self.account = sourceAccountList[1]

29 self.exchange = exchangeTicker[0]

30 self.ticker = exchangeTicker[1]

31 self.priceCondition = param["priceCondition"]

32

33

34class PriceCondition(object):

35 def __init__(self, param):

36 self.currentPrice = int(param["currentPrice"])

37 self.compare = int(param["compare"])

38 self.triggerPrice = float(param["triggerPrice"])

39

40

41def update_strategy_state(state, value, context):

42 strategy_state = lf.types.StrategyStateUpdate()

43

44 if state == lf.enums.StrategyState.Normal:

45 strategy_state.value = str(value)

46 context.log.info(str(value))

47 elif state == lf.enums.StrategyState.Warn:

48 strategy_state.value = str(value)

49 context.log.warn(str(value))

50 else:

51 strategy_state.value = str(value)

52 context.log.error(str(value))

53

54 strategy_state.state = state

55

56 context.update_strategy_state(strategy_state)

57

58

59def pre_start(context):

60 context.MIN_VOL = 0

61 context.time_trigger = False

62 context.price = -1.0

63 context.order_placed = False

64 context.log.info("参数 {}".format(context.arguments))

65 args_dict = json.loads(context.arguments)

66

67 context.config = Config(args_dict)

68 context.trigger_info = ""

69 if context.config.startTime > 0:

70 date_time_for_nano = datetime.fromtimestamp(

71 context.config.startTime / (10**9)

72 )

73 time_str = date_time_for_nano.strftime("%Y-%m-%d %H:%M:%S.%f")

74 context.trigger_info = "时间满足" + time_str

75 if (not context.config.priceCondition) and context.config.startTime == 0:

76 update_strategy_state(

77 lf.enums.StrategyState.Error,

78 "触发时间和触发价格没设置.",

79 context,

80 )

81 context.log.info("触发时间和触发价格都没设置")

82 context.req_deregister()

83 return

84 if context.config.source:

85 context.add_account(context.config.source, context.config.account)

86 context.subscribe(

87 context.config.marketSource,

88 [context.config.ticker],

89 context.config.exchange,

90 )

91

92 update_strategy_state(

93 lf.enums.StrategyState.Normal,

94 "正常",

95 context,

96 )

97

98 ins_type = wc.utils.get_instrument_type(

99 context.config.exchange, context.config.ticker

100 )

101 context.log.info("(标的类型) {}".format(ins_type))

102 if context.MIN_VOL == 0:

103 context.MIN_VOL = type_to_minvol(ins_type)

104

105

106def str_to_nanotime(tm):

107 if tm is None or tm == "" or tm == "Invalid Date":

108 return 0

109 if tm.isdigit(): # in milliseconds

110 return int(tm) * 10**6

111 else:

112 year_month_day = time.strftime("%Y-%m-%d", time.localtime())

113 ymdhms = year_month_day + " " + tm.split(" ")[1]

114 timeArray = time.strptime(ymdhms, "%Y-%m-%d %H:%M:%S")

115 nano = int(time.mktime(timeArray) * 10**9)

116 return nano

117

118

119def type_to_minvol(argument):

120 switcher = {

121 InstrumentType.Stock: int(100),

122 InstrumentType.Future: int(1),

123 InstrumentType.Bond: int(1),

124 InstrumentType.StockOption: int(1),

125 InstrumentType.Fund: int(1),

126 InstrumentType.TechStock: int(200),

127 InstrumentType.Index: int(1),

128 }

129 return switcher.get(argument, int(1))

130

131

132def place_order(context):

133 if not context.order_placed:

134 if context.price < 0:

135 update_strategy_state(

136 lf.enums.StrategyState.Warn,

137 "没有收到行情",

138 context,

139 )

140 context.log.error("没有收到行情, 无法下单, 请检查行情连接")

141 context.req_deregister()

142 return

143

144 rest_volume = context.config.volume

145 if context.config.maxLot == 0 or context.config.maxLot >= context.config.volume:

146 order_volume = rest_volume

147 else:

148 order_volume = context.config.maxLot

149 order_volume = int(

150 math.ceil(float(order_volume) / context.MIN_VOL) * context.MIN_VOL

151 )

152 i_order = 0

153 vol_list = dict()

154 now_nano = time.time_ns()

155 while rest_volume > 0:

156 i_order += 1

157 volume = (

158 order_volume

159 if order_volume <= rest_volume

160 else int(

161 math.ceil(float(rest_volume) / context.MIN_VOL) * context.MIN_VOL

162 )

163 )

164 order_id = context.insert_order(

165 context.config.ticker,

166 context.config.exchange,

167 context.config.source,

168 context.config.account,

169 context.price,

170 volume,

171 context.config.priceType,

172 context.config.side,

173 context.config.offset,

174 )

175 rest_volume -= order_volume

176 vol_list[order_id] = volume

177 context.order_placed = True

178 date_time_for_nano = datetime.fromtimestamp(now_nano / (10**9))

179 time_str = date_time_for_nano.strftime("%Y-%m-%d %H:%M:%S.%f")

180 context.log.info(

181 "-------------------- {} 开始下单 时间 {} --------------------".format(

182 context.trigger_info, time_str

183 )

184 )

185 for key, val in vol_list.items():

186 context.log.info("订单号 {}, 下单数量 {} 下单价格 {}".format(key, val, context.price))

187

188 update_strategy_state(

189 lf.enums.StrategyState.Normal,

190 "下单完成, 退出任务",

191 context,

192 )

193 context.log.info("下单完成, 退出任务")

194 context.req_deregister()

195

196

197def post_start(context):

198 start = context.config.startTime - 60000000

199

200 if context.config.startTime > 0:

201 context.add_timer(context.config.startTime, lambda ctx, event: place_order(ctx))

202

203

204def on_quote(context, quote, source_location, dest):

205 if context.config.orderPrice == "0":

206 context.price = quote.last_price

207 elif context.config.orderPrice == "1":

208 if context.config.side == Side.Buy:

209 context.price = quote.ask_price[0]

210 else:

211 context.price = quote.bid_price[0]

212 elif context.config.orderPrice == "2":

213 if context.config.side == Side.Buy:

214 context.price = quote.bid_price[0]

215 else:

216 context.price = quote.ask_price[0]

217

218 if context.config.priceCondition:

219 for i, item in enumerate(context.config.priceCondition):

220 is_price_triggerred = True

221 if item["currentPrice"] == "1":

222 quote_price = quote.bid_price[0]

223 elif item["currentPrice"] == "-1":

224 quote_price = quote.ask_price[0]

225 else:

226 quote_price = quote.last_price

227 if item["compare"] == "1":

228 is_price_triggerred = quote_price >= float(item["triggerPrice"])

229 if is_price_triggerred:

230 context.trigger_info = "价格大于等于" + str(item["triggerPrice"])

231 elif item["compare"] == "2":

232 is_price_triggerred = quote_price > float(item["triggerPrice"])

233 if is_price_triggerred:

234 context.trigger_info = "价格大于" + str(item["triggerPrice"])

235 elif item["compare"] == "3":

236 is_price_triggerred = quote_price <= float(item["triggerPrice"])

237 if is_price_triggerred:

238 context.trigger_info = "价格小于等于" + str(item["triggerPrice"])

239 elif item["compare"] == "4":

240 is_price_triggerred = quote_price < float(item["triggerPrice"])

241 if is_price_triggerred:

242 context.trigger_info = "价格小于" + str(item["triggerPrice"])

243 else:

244 return

245 if not is_price_triggerred:

246 return

247 place_order(context)

配置文件package.json

1{

2 "name": "@kungfu-trader/kfx-task-condition",

3 "author": {

4 "name": "kungfu-trader",

5 "email": "info@kungfu.link"

6 },

7 "kungfuBuild": {

8 "python": {

9 "dependencies": {}

10 }

11 },

12 "kungfuConfig": {

13 "key": "ConditionOrder",

14 "name": "条件单",

15 "ui_config": {

16 "position": "make_order"

17 },

18 "language": {

19 "zh-CN": {

20 "accountId": "账户",

21 "marketSource": "行情",

22 "ticker": "标的",

23 "side": "买卖",

24 "offset": "开平",

25 "priceType": "下单类型",

26 "priceCondition": "价格条件",

27 "currentPrice": "当前价格",

28 "currentPrice_0": "买一价",

29 "currentPrice_1": "卖一价",

30 "currentPrice_2": "最新价",

31 "compare": "比较符",

32 "triggerPrice": "触发价格",

33 "orderPrice": "下单价格",

34 "orderPrice_0": "最新价",

35 "orderPrice_1": "对手价一档",

36 "orderPrice_2": "同方向一档",

37 "volume": "数量",

38 "maxLot": "单次最大手数",

39 "maxLotTip": "柜台允许的单次最大手数, 以此为基础进行拆单, 不填则表示柜台无限制, 股票请填100的整数倍, 否则自动向下取整, 小于100则会强制设成100",

40 "startTime": "触发时间"

41 },

42 "en-US": {

43 "accountId": "Account Id",

44 "marketSource": "Market Source",

45 "ticker": "Ticker",

46 "side": "Side",

47 "offset": "Offset",

48 "priceType": "Price Type",

49 "priceCondition": "Price Condition",

50 "currentPrice": "Current Price",

51 "currentPrice_0": "Buy First Price",

52 "currentPrice_1": "Sell First Price",

53 "currentPrice_2": "Latest Price",

54 "compare": "Compare",

55 "triggerPrice": "Trigger Price",

56 "orderPrice": "Order Price",

57 "orderPrice_0": "Latest Price",

58 "orderPrice_1": "Opponent First Level Price",

59 "orderPrice_2": "Same Side First Level Price",

60 "volume": "Volume",

61 "maxLot": "Max Lot",

62 "maxLotTip": "The single max hands that counter allow, this is the basis for the dismantling of the order. If you don't fill in the form, it means the counter is unlimited. Please fill in an integer multiple of 100, otherwise it will be rounded down automatically. If it is less than 100, it will be set to 100.",

63 "startTime": "Trigger Time"

64 }

65 },

66 "config": {

67 "strategy": {

68 "type": "trade",

69 "settings": [

70 {

71 "key": "accountId",

72 "name": "ConditionOrder.accountId",

73 "type": "td",

74 "required": true,

75 "showArg": true

76 },

77 {

78 "key": "marketSource",

79 "name": "ConditionOrder.marketSource",

80 "type": "md",

81 "required": true,

82 "showArg": true

83 },

84 {

85 "key": "ticker",

86 "name": "ConditionOrder.ticker",

87 "type": "instrument",

88 "required": true,

89 "showArg": true

90 },

91 {

92 "key": "side",

93 "name": "ConditionOrder.side",

94 "type": "side",

95 "default": 0,

96 "required": true,

97 "showArg": true

98 },

99 {

100 "key": "offset",

101 "name": "ConditionOrder.offset",

102 "type": "offset",

103 "default": 0,

104 "required": true,

105 "showArg": true

106 },

107 {

108 "key": "priceType",

109 "name": "ConditionOrder.priceType",

110 "type": "priceType",

111 "default": "1",

112 "required": false

113 },

114 {

115 "key": "priceCondition",

116 "name": "ConditionOrder.priceCondition",

117 "type": "table",

118 "columns": [

119 {

120 "key": "currentPrice",

121 "name": "ConditionOrder.currentPrice",

122 "type": "select",

123 "options": [

124 {

125 "label": "ConditionOrder.currentPrice_0",

126 "value": "1"

127 },

128 {

129 "label": "ConditionOrder.currentPrice_1",

130 "value": "-1"

131 },

132 {

133 "label": "ConditionOrder.currentPrice_2",

134 "value": "0"

135 }

136 ],

137 "default": "0",

138 "required": true

139 },

140 {

141 "key": "compare",

142 "name": "ConditionOrder.compare",

143 "type": "select",

144 "options": [

145 {

146 "label": ">=",

147 "value": "1"

148 },

149 {

150 "label": ">",

151 "value": "2"

152 },

153 {

154 "label": "<=",

155 "value": "3"

156 },

157 {

158 "label": "<",

159 "value": "4"

160 }

161 ],

162 "default": "1",

163 "required": true

164 },

165 {

166 "key": "triggerPrice",

167 "name": "ConditionOrder.triggerPrice",

168 "type": "float",

169 "required": true

170 }

171 ],

172 "required": false

173 },

174 {

175 "key": "orderPrice",

176 "name": "ConditionOrder.orderPrice",

177 "type": "select",

178 "options": [

179 {

180 "label": "ConditionOrder.orderPrice_0",

181 "value": "0"

182 },

183 {

184 "label": "ConditionOrder.orderPrice_1",

185 "value": "1"

186 },

187 {

188 "label": "ConditionOrder.orderPrice_2",

189 "value": "2"

190 }

191 ],

192 "required": true

193 },

194 {

195 "key": "volume",

196 "name": "ConditionOrder.volume",

197 "type": "int",

198 "min": 0,

199 "required": true

200 },

201 {

202 "key": "maxLot",

203 "name": "ConditionOrder.maxLot",

204 "type": "int",

205 "min": 0,

206 "tip": "ConditionOrder.maxLotTip",

207 "required": false,

208 "default": 0

209 },

210 {

211 "key": "startTime",

212 "name": "ConditionOrder.startTime",

213 "type": "timePicker",

214 "required": false

215 }

216 ]

217 }

218 }

219 }

220}

说明文档 README.md

1条件单逻辑说明 :

2

3- 条件单可以接受两个类型的条件为约束,一个是价格条件,一个是时间条件

4- 当仅有价格条件时 会在当前价格满足大于小于等于触发价格时下单

5- 当仅有时间条件时 会在到达目标设定时间点时下单

6- 当价格条件跟时间条件同时存在时,哪个条件先满足,以哪个条件下单

7- 单次最大手数:若设置下单数量1000,而单比最大下单量为100,则会在下单时,拆为10份,每次100,一同下出。

2. 编译生成二进制文件

编译流程:

(1)在命令行中进入交易任务文件根目录下

$ cd kfx-task-condition-demo/

# 举例交易任务文件名为 kfx-task-condition-demo

(2)执行kfs编译命令

$ kfs extension build

注意

执行编译的kfs命令路径为功夫的安装目录下 /Kungfu/resources/kfc/kfs

举例: Windows系统下,功夫安装路径为D盘的根目录,即功夫安装目录为 D:/Kungfu

编译命令为 : D:/Kungfu/resources/kfc/kfs.exe extension build

举例: linux系统下,功夫安装路径为/opt/Kungfu

编译命令为 : /opt/Kungfu/resources/kfc/kfs extension build

编译后文件目录结构:

kfx-task-condition-demo/

├── src/

│ └── python

| └── ConditionOrder

| └── __init__.py

├── README.md

├── package.json

├── __pypackages__/ # Python模块库, 自动生成

├── dist/ # 编译打包出来的二进制文件所在文件夹

| └── ConditionOrder

| └── ConditionOrder.cp39-win_amd64.pyd # 二进制文件

├── pdm.lock # build后下载依赖库自动生成的文件

└── pyproject.toml # build后下载依赖库自动生成的文件

3. 将文件拷贝到插件目录

流程:

(1)在命令行中进入交易任务文件根目录下

$ cd kfx-task-condition-demo/

# 举例交易任务文件名为 kfx-task-condition-demo

(2)复制二进制文件所在的目录拷贝到Kungfu插件目录

注意

插件目录路径为功夫的安装目录下 /Kungfu/resources/app/kungfu-extensions/

Windows系统 : Copy-Item -Path ./dist/ConditionOrder/ -Destination D:/Kungfu/resources/app/kungfu-extensions/ConditionOrder/ -Recurse -Force

Linux系统 : cp -r ./dist/ConditionOrder/ /opt/Kungfu/resources/app/kungfu-extensions/

4. 添加交易任务

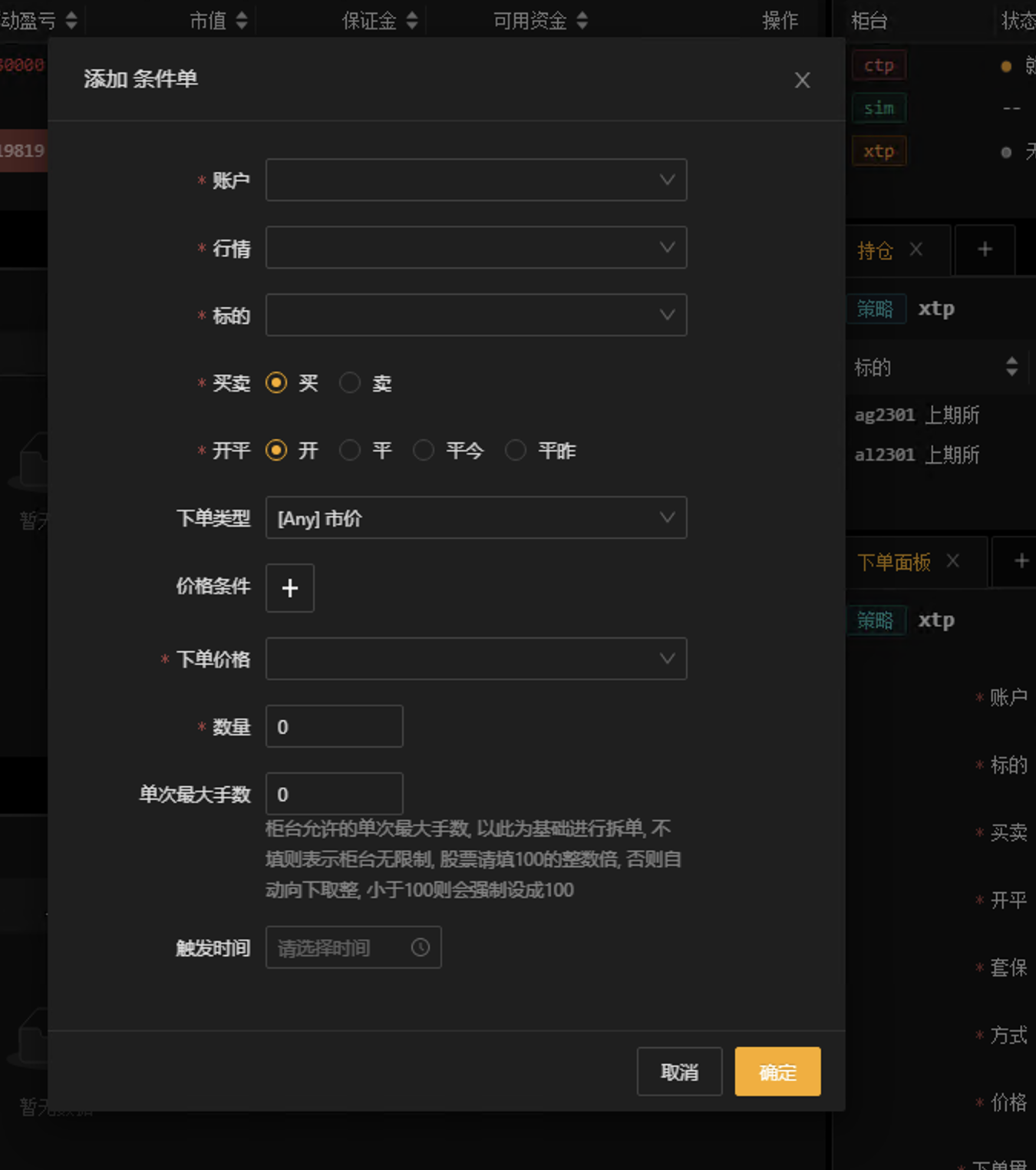

重启Kungfu图形客户端,选择主面板中的”交易任务”面板,点击右上角的”添加”按钮,在弹出的”选择交易任务”面板中选择”条件单”

交易任务和策略的区别

功能描述 |

交易任务 |

策略 |

前端参数 |

可传参(交易任务可以接收前端配置的参数,前端配置的参数会以一个json字符串格式传入到 context.arguments。) |

不可传参 |

交易进度信息统计展示 |

展示进度信息(交易任务可以在成交和委托回调中,统计成交进度,或是属于交易任务特有的指标,前端界面可以显示这些信息,同时还可以进行异常报警提示。) |

不展示 |

柜台对接

从零开始构建一个交易柜台

创建目录结构

源码目录结构:

xtp/ # xtp柜台名称

├── src/

│ └── cpp

│ ├── buffer_data.h

│ ├── exports.cpp

│ ├── marketdata_xtp.cpp

│ ├── marketdata_xtp.h

│ ├── serialize_xtp.h

│ ├── trader_xtp.cpp

│ ├── trader_xtp.h

│ └── type_convert.h

└── package.json # 编译配置信息

package.json文件

1{

2 "name": "@kungfu-trader/kfx-broker-xtp-demo",

3 "author": {

4 "name": "Kungfu Trader",

5 "email": "info@kungfu.link"

6 },

7 "version": "3.0.6-alpha.4",

8 "description": "Kungfu Extension - XTP Demo",

9 "license": "Apache-2.0",

10 "main": "package.json",

11 "repository": {

12 "url": "https://github.com/kungfu-trader/kungfu.git"

13 },

14 "publishConfig": {

15 "registry": "https://npm.pkg.github.com"

16 },

17 "binary": {

18 "module_name": "kfx-broker-xtp-demo",

19 "module_path": "dist/xtp",

20 "remote_path": "{module_name}/v{major}/v{version}",

21 "package_name": "{module_name}-v{version}-{platform}-{arch}-{configuration}.tar.gz",

22 "host": "https://prebuilt.libkungfu.cc"

23 },

24 "scripts": {

25 "build": "C:/Users/PC/Documents/kfgit/v27/kf27/artifact/build/stage/artifact-kungfu/v2/v3.0.6-alpha.4/win-unpacked/resources/kfc/kfs.exe extension build", // 替换成你的Kungfu安装目录

26 "clean": "C:/Users/PC/Documents/kfgit/v27/kf27/artifact/build/stage/artifact-kungfu/v2/v3.0.6-alpha.4/win-unpacked/resources/kfc/kfs.exe extension clean", // 替换成你的Kungfu安装目录

27 "format": "node ../../framework/core/.gyp/run-format-cpp.js src",

28 "install": "node -e \"require('@kungfu-trader/kungfu-core').prebuilt('install')\"",

29 "package": "kfs extension package"

30 },

31 "dependencies": {

32 "@kungfu-trader/kungfu-core": "^3.0.6-alpha.4"

33 },

34 "devDependencies": {

35 "@kungfu-trader/kungfu-sdk": "^3.0.6-alpha.4"

36 },

37 "kungfuDependencies": {

38 "xtp": "v2.2.37.4"

39 },

40 "kungfuBuild": {

41 "build_type": "Release",

42 "cpp": {

43 "target": "bind/python",

44 "links": {

45 "windows": [

46 "xtptraderapi",

47 "xtpquoteapi"

48 ],

49 "linux": [

50 "xtptraderapi",

51 "xtpquoteapi"

52 ],

53 "macos": [

54 "xtptraderapi",

55 "xtpquoteapi"

56 ]

57 }

58 }

59 },

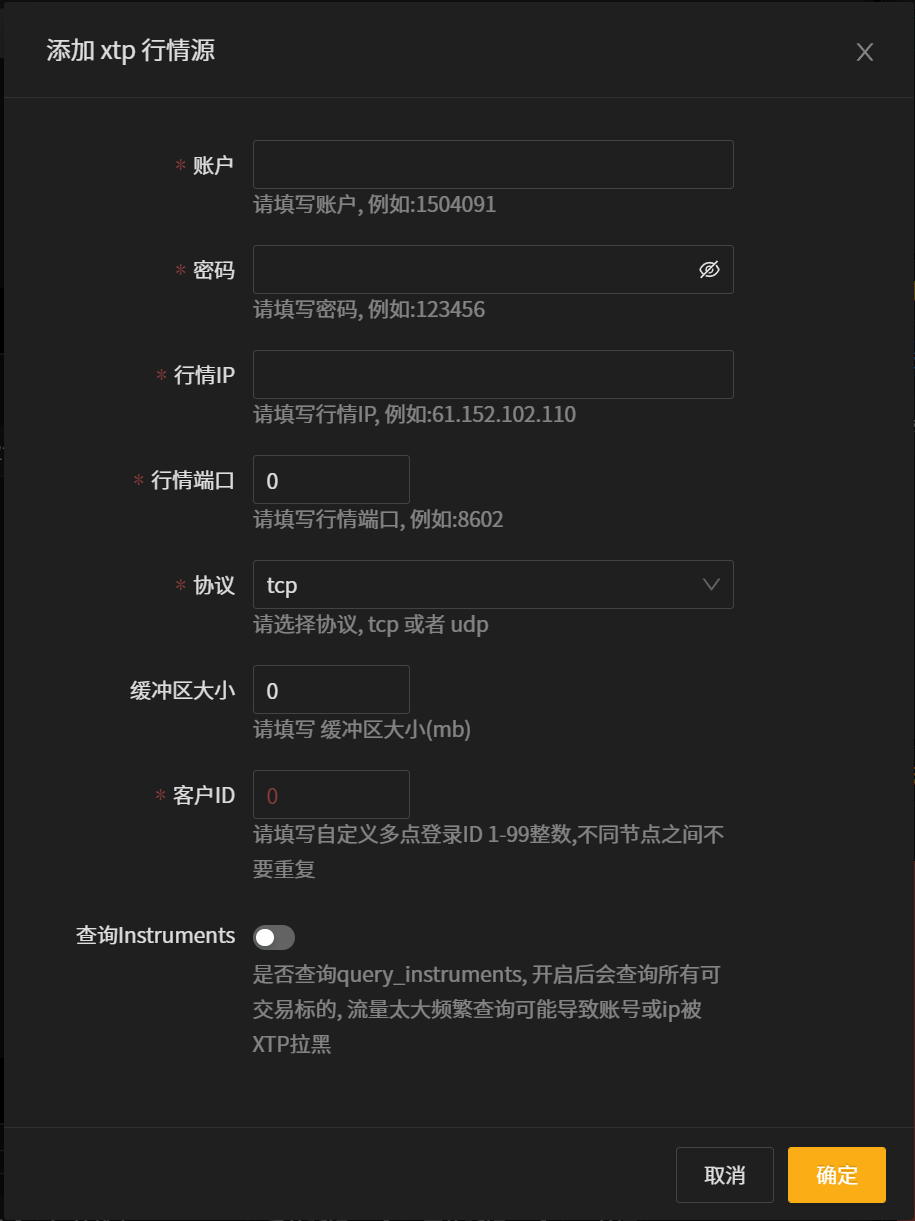

60 "kungfuConfig": {

61 "key": "xtp",

62 "name": "XTP",

63 "language": {

64 "zh-CN": {

65 "account_name": "账户别名",

66 "account_name_tip": "请填写账户别名",

67 "account_id": "账户",

68 "account_id_tip": "请填写账户, 例如:1504091",

69 "password": "密码",

70 "password_tip": "请填写密码, 例如:123456",

71 "software_key": "软件密钥",

72 "software_key_tip": "请填写软件密钥, 例如:b8aa7173bba3470e390d787219b2112",

73 "td_ip": "交易IP",

74 "td_ip_tip": "请填写交易IP, 例如:61.152.102.111",

75 "td_port": "交易端口",

76 "td_port_tip": "请填写交易端口, 例如:8601",

77 "client_id": "客户ID",

78 "client_id_tip": "请填写自定义多点登录ID 1-99整数,不同节点之间不要重复",

79 "md_ip": "行情IP",

80 "md_ip_tip": "请填写行情IP, 例如:61.152.102.110",

81 "md_port": "行情端口",

82 "md_port_tip": "请填写行情端口, 例如:8602",

83 "protocol": "协议",

84 "protocol_tip": "请选择协议, tcp 或者 udp",

85 "buffer_size": "缓冲区大小",

86 "buffer_size_tip": "请填写 缓冲区大小(mb)",

87 "sync_external_order": "同步外部订单",

88 "sync_external_order_msg": "是否同步外部订单",

89 "sync_external_order_tip": "若开启则同步用户在其他交易软件的订单",

90 "recover_order_trade": "恢复订单",

91 "recover_order_trade_msg": "启动时是否查询恢复订单",

92 "recover_order_trade_tip": "若开启则启动时查询今日委托和成交",

93 "query_instruments": "查询可交易标的",

94 "query_instruments_tip": "是否查询可交易标的, 开启后会查询所有可交易标的, 流量太大频繁查询可能导致账号或ip被XTP拉黑"

95 },

96 "en-US": {

97 "account_name": "account name",

98 "account_name_tip": "Please enter account name",

99 "account_id": "account id",

100 "account_id_tip": "Please enter account id",

101 "password": "password",

102 "password_tip": "Please enter password, for example:123456",

103 "software_key": "software key",

104 "software_key_tip": "Please enter software key, for example :b8aa7173bba3470e390d787219b2112",

105 "td_ip": "td IP",

106 "td_ip_tip": "Please enter td IP, for example:61.152.102.111",

107 "td_port": "td port",

108 "td_port_tip": "Please enter td port, for example:8601",

109 "client_id": "client id",

110 "client_id_tip": "Please enter t user-defined multipoint client ID, which is an integer ranging from 1 to 99. The value must be unique on different nodes",

111 "md_ip": "md IP",

112 "md_ip_tip": "Please enter md IP, for example :61.152.102.110",

113 "md_port": "md port",

114 "md_port_tip": "Please enter md port, for example:8602",

115 "protocol": "protocol",

116 "protocol_tip": "Please select protocol, tcp or udp",

117 "buffer_size": "buffer size",

118 "buffer_size_tip": "Please enter buffer size(mb)",

119 "sync_external_order": "sync external order",

120 "sync_external_order_msg": "Whether open sync_external_order",

121 "sync_external_order_tip": "If enabled, it synchronizes users' orders in other trading software",

122 "recover_order_trade": "recover order trade",

123 "recover_order_trade_msg": "Whether recover order trade",

124 "recover_order_trade_tip": "If enabled, query order and trade when TD ready",

125 "query_instruments": "query instruments",

126 "query_instruments_tip": "If enabled, query instruments. too much infomation may result in account or ip blacklisted by XTP"

127 }

128 },

129 "config": {

130 "td": {

131 "type": [

132 "stock"

133 ],

134 "settings": [

135 {

136 "key": "account_name",

137 "name": "xtp.account_name",

138 "type": "str",

139 "tip": "xtp.account_name_tip"

140 },

141 {

142 "key": "account_id",

143 "name": "xtp.account_id",

144 "type": "str",

145 "required": true,

146 "primary": true,

147 "tip": "xtp.account_id_tip"

148 },

149 {

150 "key": "password",

151 "name": "xtp.password",

152 "type": "password",

153 "required": true,

154 "tip": "xtp.password_tip"

155 },

156 {

157 "key": "software_key",

158 "name": "xtp.software_key",

159 "type": "str",

160 "required": true,

161 "tip": "xtp.software_key_tip"

162 },

163 {

164 "key": "td_ip",

165 "name": "xtp.td_ip",

166 "type": "str",

167 "required": true,

168 "tip": "xtp.td_ip_tip"

169 },

170 {

171 "key": "td_port",

172 "name": "xtp.td_port",

173 "type": "int",

174 "required": true,

175 "tip": "xtp.td_port_tip"

176 },

177 {

178 "key": "client_id",

179 "name": "xtp.client_id",

180 "type": "int",

181 "required": true,

182 "tip": "xtp.client_id_tip"

183 },

184 {

185 "key": "sync_external_order",

186 "name": "xtp.sync_external_order",

187 "type": "bool",

188 "errMsg": "xtp.sync_external_order_msg",

189 "required": false,

190 "default": false,

191 "tip": "xtp.sync_external_order_tip"

192 },

193 {

194 "key": "recover_order_trade",

195 "name": "xtp.recover_order_trade",

196 "type": "bool",

197 "errMsg": "xtp.recover_order_trade_msg",

198 "required": false,

199 "default": false,

200 "tip": "xtp.recover_order_trade_tip"

201 }

202 ]

203 },

204 "md": {

205 "type": [

206 "stock"

207 ],

208 "settings": [

209 {

210 "key": "account_id",

211 "name": "xtp.account_id",

212 "type": "str",

213 "required": true,

214 "tip": "xtp.account_id_tip",

215 "default": "15011218"

216 },

217 {

218 "key": "password",

219 "name": "xtp.password",

220 "type": "password",

221 "required": true,

222 "tip": "xtp.password_tip",

223 "default": "PsVqy99v"

224 },

225 {

226 "key": "md_ip",

227 "name": "xtp.md_ip",

228 "type": "str",

229 "required": true,

230 "tip": "xtp.md_ip_tip",

231 "default": "119.3.103.38"

232 },

233 {

234 "key": "md_port",

235 "name": "xtp.md_port",

236 "type": "int",

237 "required": true,

238 "tip": "xtp.md_port_tip",

239 "default": 6002

240 },

241 {

242 "key": "protocol",

243 "name": "xtp.protocol",

244 "type": "select",

245 "options": [

246 {

247 "value": "tcp",

248 "label": "tcp"

249 },

250 {

251 "value": "udp",

252 "label": "udp"

253 }

254 ],

255 "required": false,

256 "tip": "xtp.protocol_tip",

257 "default": "tcp"

258 },

259 {

260 "key": "buffer_size",

261 "name": "xtp.buffer_size",

262 "type": "int",

263 "tip": "xtp.buffer_size_tip",

264 "required": false

265 },

266 {

267 "key": "client_id",

268 "name": "xtp.client_id",

269 "type": "int",

270 "required": true,

271 "tip": "xtp.client_id_tip",

272 "default": 23

273 },

274 {

275 "key": "query_instruments",

276 "name": "xtp.query_instruments",

277 "type": "bool",

278 "required": false,

279 "tip": "xtp.query_instruments_tip",

280 "default": false

281 }

282 ]

283 }

284 }

285 }

286}

serialize_xtp.h文件

XTP数据结构添加to_stirng方便打印日志查看数据

1#ifndef KUNGFU_SERIALIZE_XTP_H

2#define KUNGFU_SERIALIZE_XTP_H

3#include <nlohmann/json.hpp>

4#include <xtp_api_struct.h>

5namespace nlohmann {

6NLOHMANN_DEFINE_TYPE_NON_INTRUSIVE(XTPQueryOrderRsp, order_xtp_id, order_client_id, order_cancel_client_id,

7 order_cancel_xtp_id, ticker, market, price, quantity, price_type, side,

8 position_effect, reserved1, reserved2, business_type, qty_traded, qty_left,

9 insert_time, update_time, cancel_time, trade_amount, order_local_id, order_status,

10 order_submit_status, order_type);

11NLOHMANN_DEFINE_TYPE_NON_INTRUSIVE(XTPOrderInsertInfo, order_xtp_id, order_client_id, ticker, market, price, stop_price,

12 quantity, price_type, side, position_effect, reserved1, reserved2, business_type);

13NLOHMANN_DEFINE_TYPE_NON_INTRUSIVE(XTPTradeReport, order_xtp_id, order_client_id, ticker, market, local_order_id,

14 exec_id, price, quantity, trade_time, trade_amount, report_index, order_exch_id,

15 trade_type, side, position_effect, reserved1, reserved2, business_type, branch_pbu);

16NLOHMANN_DEFINE_TYPE_NON_INTRUSIVE(XTPOrderCancelInfo, order_cancel_xtp_id, order_xtp_id);

17NLOHMANN_DEFINE_TYPE_NON_INTRUSIVE(XTPQueryStkPositionRsp, ticker, ticker_name, market, total_qty, sellable_qty,

18 avg_price, unrealized_pnl, yesterday_position, purchase_redeemable_qty,

19 position_direction, position_security_type, executable_option, lockable_position,

20 executable_underlying, locked_position, usable_locked_position, profit_price,

21 buy_cost, profit_cost, unknown);

22NLOHMANN_DEFINE_TYPE_NON_INTRUSIVE(XTPQueryAssetRsp, total_asset, buying_power, security_asset, fund_buy_amount,

23 fund_buy_fee, fund_sell_amount, fund_sell_fee, withholding_amount, account_type,

24 frozen_margin, frozen_exec_cash, frozen_exec_fee, pay_later, preadva_pay,

25 orig_banlance, banlance, deposit_withdraw, trade_netting, captial_asset,

26 force_freeze_amount, preferred_amount, repay_stock_aval_banlance,

27 exchange_cur_risk_degree, company_cur_risk_degree, unknown);

28NLOHMANN_DEFINE_TYPE_NON_INTRUSIVE(XTPMarketDataStruct, exchange_id, ticker, last_price, pre_close_price, open_price,

29 high_price, low_price, close_price, pre_total_long_positon, total_long_positon,

30 pre_settl_price, settl_price, upper_limit_price, lower_limit_price, pre_delta,

31 curr_delta, data_time, qty, turnover, avg_price, bid, ask, bid_qty, ask_qty,

32 trades_count, ticker_status);

33NLOHMANN_DEFINE_TYPE_NON_INTRUSIVE(XTPRspInfoStruct, error_id, error_msg);

34NLOHMANN_DEFINE_TYPE_NON_INTRUSIVE(XTPOrderInfoEx, order_xtp_id, order_client_id, order_cancel_client_id,

35 order_cancel_xtp_id, ticker, market, price, quantity, price_type, business_type,

36 qty_traded, qty_left, insert_time, update_time, cancel_time, trade_amount,

37 order_local_id, order_status, order_submit_status, order_type, order_exch_id,

38 order_err_t, unknown);

39NLOHMANN_DEFINE_TYPE_NON_INTRUSIVE(XTPSpecificTickerStruct, exchange_id, ticker);

40} // namespace nlohmann

41namespace kungfu::wingchun::xtp {

42template <typename T> std::string to_string(const T &ori) {

43 nlohmann::json j;

44 to_json(j, ori);

45 return j.dump();

46}

47} // namespace kungfu::wingchun::xtp

48#endif

type_convert.h文件

XTP和Kungfu数据结构的转换

1#ifndef KUNGFU_XTP_EXT_TYPE_CONVERT_H

2#define KUNGFU_XTP_EXT_TYPE_CONVERT_H

3

4#include <cstddef>

5#include <cstdio>

6#include <cstring>

7#include <ctime>

8#include <kungfu/longfist/longfist.h>

9#include <kungfu/wingchun/common.h>

10#include <kungfu/yijinjing/time.h>

11#include <nlohmann/json.hpp>

12#include <xtp_api_struct.h>

13

14using namespace kungfu::longfist;

15using namespace kungfu::longfist::enums;

16using namespace kungfu::longfist::types;

17

18namespace kungfu::wingchun::xtp {

19

20template <typename T> inline void set_offset(T &t) {

21 switch (t.side) {

22 case Side::Buy:

23 t.offset = Offset::Open;

24 break;

25 case Side::Sell:

26 t.offset = Offset::Close;

27 break;

28 default:

29 SPDLOG_ERROR("Invalidated kf_side : {} ", t.side);

30 break;

31 }

32}

33

34inline XTP_PROTOCOL_TYPE get_xtp_protocol_type(const std::string &p) {

35 if (p == "udp") {

36 return XTP_PROTOCOL_UDP;

37 } else {

38 return XTP_PROTOCOL_TCP;

39 }

40}

41

42inline int64_t nsec_from_xtp_timestamp(int64_t xtp_time) {

43 std::tm result = {};

44 result.tm_year = xtp_time / (int64_t)1e13 - 1900;

45 result.tm_mon = xtp_time % (int64_t)1e13 / (int64_t)1e11 - 1;

46 result.tm_mday = xtp_time % (int64_t)1e11 / (int64_t)1e9;

47 result.tm_hour = xtp_time % (int64_t)1e9 / (int64_t)1e7;

48 result.tm_min = xtp_time % (int)1e7 / (int)1e5;

49 result.tm_sec = xtp_time % (int)1e5 / (int)1e3;

50 int milli_sec = xtp_time % (int)1e3;

51 std::time_t parsed_time = std::mktime(&result);

52 return parsed_time * kungfu::yijinjing::time_unit::NANOSECONDS_PER_SECOND +

53 milli_sec * kungfu::yijinjing::time_unit::NANOSECONDS_PER_MILLISECOND;

54}

55

56inline void from_xtp(const XTP_MARKET_TYPE &xtp_market_type, char *exchange_id) {

57 if (xtp_market_type == XTP_MKT_SH_A) {

58 strcpy(exchange_id, "SSE");

59 } else if (xtp_market_type == XTP_MKT_SZ_A) {

60 strcpy(exchange_id, "SZE");

61 }

62}

63

64inline void to_xtp(XTP_MARKET_TYPE &xtp_market_type, const char *exchange_id) {

65 if (!strcmp(exchange_id, "SSE")) {

66 xtp_market_type = XTP_MKT_SH_A;

67 } else if (!strcmp(exchange_id, "SZE")) {

68 xtp_market_type = XTP_MKT_SZ_A;

69 } else {

70 xtp_market_type = XTP_MKT_UNKNOWN;

71 }

72}

73

74inline std::string exchange_id_from_xtp(const XTP_EXCHANGE_TYPE ex) {

75 if (ex == XTP_EXCHANGE_SH) {

76 return EXCHANGE_SSE;

77 } else if (ex == XTP_EXCHANGE_SZ) {

78 return EXCHANGE_SZE;

79 } else {

80 return "Unknown";

81 }

82}

83

84inline void from_xtp(const XTP_EXCHANGE_TYPE &xtp_exchange_type, char *exchange_id) {

85 if (xtp_exchange_type == XTP_EXCHANGE_SH) {

86 strcpy(exchange_id, "SSE");

87 } else if (xtp_exchange_type == XTP_EXCHANGE_SZ) {

88 strcpy(exchange_id, "SZE");

89 }

90}

91

92inline void to_xtp_exchange(XTP_EXCHANGE_TYPE &xtp_exchange_type, const char *exchange_id) {

93 if (strcmp(exchange_id, "SSE") == 0) {

94 xtp_exchange_type = XTP_EXCHANGE_SH;

95 } else if (strcmp(exchange_id, "SZE") == 0) {

96 xtp_exchange_type = XTP_EXCHANGE_SZ;

97 } else {

98 xtp_exchange_type = XTP_EXCHANGE_UNKNOWN;

99 }

100}

101

102inline void from_xtp(const XTP_PRICE_TYPE &xtp_price_type, const XTP_MARKET_TYPE &xtp_exchange_type,

103 PriceType &price_type) {

104 if (xtp_price_type == XTP_PRICE_LIMIT)

105 price_type = PriceType::Limit;

106 else if (xtp_price_type == XTP_PRICE_BEST5_OR_CANCEL)

107 price_type = PriceType::FakBest5;

108 else if (xtp_exchange_type == XTP_MKT_SH_A) {

109 if (xtp_price_type == XTP_PRICE_BEST5_OR_LIMIT)

110 price_type = PriceType::ReverseBest;

111 } else if (xtp_exchange_type == XTP_MKT_SZ_A) {

112 if (xtp_price_type == XTP_PRICE_BEST_OR_CANCEL)

113 price_type = PriceType::Fak;

114 else if (xtp_price_type == XTP_PRICE_FORWARD_BEST)

115 price_type = PriceType::ForwardBest;

116 else if (xtp_price_type == XTP_PRICE_REVERSE_BEST_LIMIT)

117 price_type = PriceType::ReverseBest;

118 else if (xtp_price_type == XTP_PRICE_ALL_OR_CANCEL)

119 price_type = PriceType::Fok;

120 } else

121 price_type = PriceType::Unknown;

122}

123

124inline void to_xtp(XTP_PRICE_TYPE &xtp_price_type, const PriceType &price_type, const char *exchange) {

125 if (price_type == PriceType::Limit)

126 xtp_price_type = XTP_PRICE_LIMIT;

127 else if ((price_type == PriceType::Any) || (price_type == PriceType::FakBest5))

128 xtp_price_type = XTP_PRICE_BEST5_OR_CANCEL;

129 else if (strcmp(exchange, EXCHANGE_SSE) == 0) {

130 if (price_type == PriceType::ReverseBest)

131 xtp_price_type = XTP_PRICE_BEST5_OR_LIMIT;

132 } else if (strcmp(exchange, EXCHANGE_SZE) == 0) {

133 if (price_type == PriceType::Fak)

134 xtp_price_type = XTP_PRICE_BEST_OR_CANCEL;

135 else if (price_type == PriceType::ForwardBest)

136 xtp_price_type = XTP_PRICE_FORWARD_BEST;

137 else if (price_type == PriceType::ReverseBest)

138 xtp_price_type = XTP_PRICE_REVERSE_BEST_LIMIT;

139 else if (price_type == PriceType::Fok)

140 xtp_price_type = XTP_PRICE_ALL_OR_CANCEL;

141 } else

142 xtp_price_type = XTP_PRICE_TYPE_UNKNOWN;

143}

144

145inline void from_xtp(const XTP_ORDER_STATUS_TYPE &xtp_order_status, OrderStatus &status) {

146 if (xtp_order_status == XTP_ORDER_STATUS_INIT || xtp_order_status == XTP_ORDER_STATUS_NOTRADEQUEUEING) {

147 status = OrderStatus::Pending;

148 } else if (xtp_order_status == XTP_ORDER_STATUS_ALLTRADED) {

149 status = OrderStatus::Filled;

150 } else if (xtp_order_status == XTP_ORDER_STATUS_CANCELED) {

151 status = OrderStatus::Cancelled;

152 } else if (xtp_order_status == XTP_ORDER_STATUS_PARTTRADEDQUEUEING) {

153 status = OrderStatus::PartialFilledActive;

154 } else if (xtp_order_status == XTP_ORDER_STATUS_PARTTRADEDNOTQUEUEING) {

155 status = OrderStatus::PartialFilledNotActive;

156 } else if (xtp_order_status == XTP_ORDER_STATUS_REJECTED) {

157 status = OrderStatus::Error;

158 } else {

159 status = OrderStatus::Unknown;

160 }

161}

162

163inline void from_xtp(XTPQSI *ticker_info, Instrument &instrument) {

164 instrument.instrument_id = ticker_info->ticker;

165 if (ticker_info->exchange_id == 1) {

166 instrument.exchange_id = EXCHANGE_SSE;

167 } else if (ticker_info->exchange_id == 2) {

168 instrument.exchange_id = EXCHANGE_SZE;

169 } else {

170 instrument.exchange_id = "unknown";

171 }

172 memcpy(instrument.product_id, ticker_info->ticker_name, strlen(ticker_info->ticker_name));

173 instrument.instrument_type = get_instrument_type(instrument.exchange_id, instrument.instrument_id);

174 instrument.price_tick = ticker_info->price_tick;

175}

176

177inline void from_xtp(const XTP_SIDE_TYPE &xtp_side, Side &side) {

178 if (xtp_side == XTP_SIDE_BUY) {

179 side = Side::Buy;

180 } else if (xtp_side == XTP_SIDE_SELL) {

181 side = Side::Sell;

182 }

183}

184

185inline void to_xtp(XTP_SIDE_TYPE &xtp_side, const Side &side) {

186 if (side == Side::Buy) {

187 xtp_side = XTP_SIDE_BUY;

188 } else if (side == Side::Sell) {

189 xtp_side = XTP_SIDE_SELL;

190 }

191}

192

193inline void to_xtp(XTPMarketDataStruct &des, const Quote &ori) {

194 // TODO

195}

196

197inline void from_xtp(const XTPMarketDataStruct &ori, Quote &des) {

198 des.data_time = nsec_from_xtp_timestamp(ori.data_time);

199 des.instrument_id = ori.ticker;

200 from_xtp(ori.exchange_id, des.exchange_id);

201

202 des.instrument_type = ori.data_type != XTP_MARKETDATA_OPTION

203 ? get_instrument_type(des.exchange_id, des.instrument_id)

204 : InstrumentType::StockOption;

205

206 des.last_price = ori.last_price;

207 des.pre_settlement_price = ori.pre_settl_price;

208 des.pre_close_price = ori.pre_close_price;

209 des.open_price = ori.open_price;

210 des.high_price = ori.high_price;

211 des.low_price = ori.low_price;

212 des.volume = ori.qty;

213 des.turnover = ori.turnover;

214 des.close_price = ori.close_price;

215 des.settlement_price = ori.settl_price;

216 des.upper_limit_price = ori.upper_limit_price;

217 des.lower_limit_price = ori.lower_limit_price;

218 des.total_trade_num = ori.trades_count;

219

220 memcpy(des.ask_price, ori.ask, sizeof(des.ask_price));

221 memcpy(des.bid_price, ori.bid, sizeof(des.ask_price));

222 for (std::size_t i = 0; i < 10; i++) {

223 des.ask_volume[i] = ori.ask_qty[i];

224 des.bid_volume[i] = ori.bid_qty[i];

225 }

226}

227

228inline void to_xtp(XTPOrderInsertInfo &des, const OrderInput &ori) {

229 strcpy(des.ticker, ori.instrument_id);

230 to_xtp(des.market, ori.exchange_id);

231 des.price = ori.limit_price;

232 des.quantity = ori.volume;

233 to_xtp(des.side, ori.side);

234 to_xtp(des.price_type, ori.price_type, ori.exchange_id);

235 des.business_type = XTP_BUSINESS_TYPE_CASH;

236}

237

238inline void from_xtp(const XTPOrderInsertInfo &ori, OrderInput &des) {

239 // TODO

240}

241

242inline void from_xtp(const XTPOrderInfo &ori, Order &des) {

243 des.instrument_id = ori.ticker;

244 from_xtp(ori.market, des.exchange_id);

245 from_xtp(ori.price_type, ori.market, des.price_type);

246 des.volume = ori.quantity;

247 des.volume_left = ori.quantity - ori.qty_traded;

248 des.limit_price = ori.price;

249 from_xtp(ori.order_status, des.status);

250 from_xtp(ori.side, des.side);

251 set_offset(des);

252 des.instrument_type = get_instrument_type(des.exchange_id, des.instrument_id);

253 if (ori.update_time > 0) {

254 des.update_time = nsec_from_xtp_timestamp(ori.update_time);

255 }

256 std::string str_external_order_id = std::to_string(ori.order_xtp_id);

257 des.external_order_id = str_external_order_id.c_str();

258}

259

260inline void from_xtp(const XTPQueryOrderRsp &ori, HistoryOrder &des) {

261 des.instrument_id = ori.ticker;

262 from_xtp(ori.market, des.exchange_id);

263 from_xtp(ori.price_type, ori.market, des.price_type);

264 des.volume = ori.quantity;

265 des.volume_left = ori.qty_left;

266 des.limit_price = ori.price;

267 from_xtp(ori.order_status, des.status);

268 from_xtp(ori.side, des.side);

269 set_offset(des);

270 des.instrument_type = get_instrument_type(des.exchange_id, des.instrument_id);

271 if (ori.update_time > 0) {

272 des.update_time = nsec_from_xtp_timestamp(ori.update_time);

273 }

274 des.external_order_id, std::to_string(ori.order_xtp_id).c_str();

275}

276

277inline void from_xtp_no_price_type(const XTPOrderInfo &ori, Order &des) {

278 des.instrument_id = ori.ticker;

279 from_xtp(ori.market, des.exchange_id);

280 des.volume = ori.quantity;

281 des.volume_left = ori.quantity - ori.qty_traded;

282 des.limit_price = ori.price;

283 from_xtp(ori.order_status, des.status);

284 from_xtp(ori.side, des.side);

285 set_offset(des);

286 des.instrument_type = get_instrument_type(des.exchange_id, des.instrument_id);

287 if (ori.update_time > 0) {

288 des.update_time = nsec_from_xtp_timestamp(ori.update_time);

289 }

290 std::string str_external_order_id = std::to_string(ori.order_xtp_id);

291 des.external_order_id = str_external_order_id.c_str();

292}

293

294inline void from_xtp(const XTPTradeReport &ori, Trade &des) {

295 des.instrument_id = ori.ticker;

296 des.volume = ori.quantity;

297 des.price = ori.price;

298 from_xtp(ori.market, des.exchange_id);

299 des.instrument_type = get_instrument_type(des.exchange_id, des.instrument_id);

300 from_xtp(ori.side, des.side);

301 set_offset(des);

302 des.trade_time = yijinjing::time::now_in_nano();

303 des.external_order_id = std::to_string(ori.order_xtp_id).c_str();

304 des.external_trade_id = ori.exec_id;

305}

306

307inline void from_xtp(const XTPQueryTradeRsp &ori, HistoryTrade &des) {

308 des.instrument_id = ori.ticker;

309 des.volume = ori.quantity;

310 des.price = ori.price;

311 from_xtp(ori.market, des.exchange_id);

312 from_xtp(ori.side, des.side);

313 // des.offset = Offset::Open;

314 set_offset(des);

315 des.instrument_type = get_instrument_type(des.exchange_id, des.instrument_id);

316 des.trade_time = nsec_from_xtp_timestamp(ori.trade_time);

317 des.external_order_id = std::to_string(ori.order_xtp_id).c_str();

318 des.external_trade_id = ori.exec_id;

319}

320

321inline void from_xtp(const XTPQueryStkPositionRsp &ori, Position &des) {

322 des.instrument_id = ori.ticker;

323 from_xtp(ori.market, des.exchange_id);

324 des.volume = ori.total_qty;

325 des.yesterday_volume = ori.sellable_qty;

326 des.avg_open_price = ori.avg_price;

327 des.position_cost_price = ori.avg_price;

328 des.static_yesterday = ori.yesterday_position;

329 // des.open_volume // 数据不足以算出该字段, 保持为0

330 // des.frozen_yesterday // 数据不足以算出该字段, 保持为0

331 // des.frozen_total // 数据不足以算出该字段, 保持为0

332}

333

334inline void from_xtp(const XTPQueryAssetRsp &ori, Asset &des) { des.avail = ori.buying_power; }

335

336inline void from_xtp(const XTPTickByTickStruct &ori, Entrust &des) {

337 from_xtp(ori.exchange_id, des.exchange_id);

338 des.instrument_id = ori.ticker;

339 des.data_time = nsec_from_xtp_timestamp(ori.data_time);

340

341 des.price = ori.entrust.price;

342 des.volume = ori.entrust.qty;

343 des.main_seq = ori.entrust.channel_no;

344 des.seq = ori.entrust.seq;

345

346 if (ori.entrust.ord_type == '1') {

347 des.price_type = PriceType::Any;

348 } else if (ori.entrust.ord_type == '2') {

349 des.price_type = PriceType::Limit;

350 } else if (ori.entrust.ord_type == 'U') {

351 des.price_type = PriceType::ForwardBest;

352 }

353

354 // xtp(深交所的order_no在xtp接口注释标注为无意义,偶尔为0 seq对应的是真正的订单号 上交所的order_no是订单号)

355 if (strcmp(des.exchange_id, "SSE")) {

356 des.orig_order_no = ori.entrust.order_no;

357 } else {

358 des.orig_order_no = ori.entrust.seq;

359 }

360

361 switch (ori.entrust.side) {

362 case 'B': {

363 des.side = Side::Buy;

364 break;

365 }

366 case 'S': {

367 des.side = Side::Sell;

368 break;

369 }

370 case '1': {

371 des.side = Side::Buy;

372 break;

373 }

374 case '2': {

375 des.side = Side::Sell;

376 break;

377 }

378 default: {

379 des.side = Side::Unknown;

380 break;

381 }

382 }

383}

384

385inline void from_xtp(const XTPTickByTickStruct &ori, Transaction &des) {

386 from_xtp(ori.exchange_id, des.exchange_id);

387 des.instrument_id = ori.ticker;

388 des.data_time = nsec_from_xtp_timestamp(ori.data_time);

389

390 if (ori.type == XTP_TBT_ENTRUST) {

391 des.instrument_id = ori.ticker;

392 des.data_time = nsec_from_xtp_timestamp(ori.data_time);

393

394 des.main_seq = ori.entrust.channel_no;

395 des.seq = ori.entrust.seq;

396

397 des.price = ori.entrust.price;

398 des.volume = ori.entrust.qty;

399

400 if (ori.entrust.side == 'B') {

401 des.side = Side::Buy;

402 des.bid_no = ori.entrust.order_no;

403 } else {

404 des.side = Side::Sell;

405 des.ask_no = ori.entrust.order_no;

406 }

407 des.exec_type = ExecType::Cancel;

408

409 } else {

410

411 des.main_seq = ori.trade.channel_no;

412 des.seq = ori.trade.seq;

413

414 des.price = ori.trade.price;

415 des.volume = ori.trade.qty;

416

417 des.bid_no = ori.trade.bid_no;

418 des.ask_no = ori.trade.ask_no;

419

420 switch (ori.trade.trade_flag) {

421 case 'B': {

422 des.side = Side::Buy;

423 des.exec_type = ExecType::Trade;

424 break;

425 }

426 case 'S': {

427 des.side = Side::Sell;

428 des.exec_type = ExecType::Trade;

429 break;

430 }

431 case 'N': {

432 des.side = Side::Unknown;

433 des.exec_type = ExecType::Trade;

434 break;

435 }

436 case '4': {

437 des.side = (des.bid_no < des.ask_no) ? Side::Sell : Side::Buy;

438 des.exec_type = ExecType::Cancel;

439 break;

440 }

441 case 'F': {

442 des.side = (des.bid_no < des.ask_no) ? Side::Sell : Side::Buy;

443 des.exec_type = ExecType::Trade;

444 break;

445 }

446 default: {

447 break;

448 }

449 }

450 }

451}

452} // namespace kungfu::wingchun::xtp

453#endif // KUNGFU_XTP_EXT_TYPE_CONVERT_H

buffer_data.h文件

封装xtp回调函数参数, 方便落地原始数据到journal

1#ifndef XTP_BUFFER_DATA_H

2#define XTP_BUFFER_DATA_H

3

4#include "serialize_xtp.h"

5

6static constexpr int32_t kXTPOrderInfoType = 12340001;

7static constexpr int32_t kXTPTradeReportType = 12340002;

8static constexpr int32_t kQueryXTPOrderInfoType = 12340003;

9static constexpr int32_t kQueryXTPTradeReportType = 12340004;

10static constexpr int32_t kCancelOrderErrorType = 12340005;

11

12static constexpr int32_t kQueryAssetType = 12340011;

13static constexpr int32_t kQueryPositionType = 12340012;

14

15struct BufferXTPTradeReport {

16 XTPQueryTradeRsp trade_info;

17 XTPRI error_info;

18 int request_id;

19 bool is_last;

20 uint64_t session_id;

21};

22

23struct BufferXTPOrderInfo {

24 XTPOrderInfo order_info;

25 XTPRI error_info;

26 int request_id;

27 bool is_last;

28 uint64_t session_id;

29};

30

31struct BufferXTPOrderCancelInfo {

32 XTPOrderCancelInfo cancel_info;

33 XTPRI error_info;

34 uint64_t session_id;

35};

36

37struct BufferXTPQueryAssetRsp {

38 XTPQueryAssetRsp asset;

39 XTPRI error_info;

40 int request_id;

41 bool is_last;

42 uint64_t session_id;

43};

44

45struct BufferXTPQueryStkPositionRsp {

46 XTPQueryStkPositionRsp position;

47 XTPRI error_info;

48 int request_id;

49 bool is_last;

50 uint64_t session_id;

51};

52

53namespace nlohmann {

54NLOHMANN_DEFINE_TYPE_NON_INTRUSIVE(BufferXTPTradeReport, trade_info, session_id, error_info, request_id, is_last);

55NLOHMANN_DEFINE_TYPE_NON_INTRUSIVE(BufferXTPOrderInfo, order_info, session_id, error_info, request_id, is_last);

56NLOHMANN_DEFINE_TYPE_NON_INTRUSIVE(BufferXTPOrderCancelInfo, cancel_info, error_info, session_id);

57NLOHMANN_DEFINE_TYPE_NON_INTRUSIVE(BufferXTPQueryAssetRsp, asset, error_info, session_id, request_id, is_last);

58NLOHMANN_DEFINE_TYPE_NON_INTRUSIVE(BufferXTPQueryStkPositionRsp, position, error_info, session_id, request_id, is_last);

59

60} // namespace nlohmann

61

62#endif // XTP_BUFFER_DATA_H

trader_xtp.h文件

xtp的交易柜台头文件定义

1#ifndef KUNGFU_XTP_EXT_TRADER_H

2#define KUNGFU_XTP_EXT_TRADER_H

3

4#include <kungfu/wingchun/broker/trader.h>

5#include <xtp_trader_api.h>

6

7namespace kungfu::wingchun::xtp {

8using namespace kungfu::longfist;

9using namespace kungfu::longfist::types;

10

11struct TDConfiguration {

12int client_id;

13std::string account_id;

14std::string password;

15std::string software_key;

16std::string td_ip;

17int td_port;

18bool sync_external_order;

19bool recover_order_trade;

20};

21

22inline void from_json(const nlohmann::json &j, TDConfiguration &c) {

23j.at("client_id").get_to(c.client_id);

24j.at("account_id").get_to(c.account_id);

25j.at("password").get_to(c.password);

26j.at("software_key").get_to(c.software_key);

27j.at("td_ip").get_to(c.td_ip);

28j.at("td_port").get_to(c.td_port);

29c.sync_external_order = j.value<bool>("sync_external_order", false);

30c.recover_order_trade = j.value<bool>("recover_order_trade", true);

31}

32

33class TraderXTP : public XTP::API::TraderSpi, public broker::Trader {

34public:

35explicit TraderXTP(broker::BrokerVendor &vendor);

36

37~TraderXTP() override;

38

39[[nodiscard]] longfist::enums::AccountType get_account_type() const override {

40 return longfist::enums::AccountType::Stock;

41}

42

43void pre_start() override;

44

45void on_start() override;

46

47void on_exit() override;

48

49bool insert_order(const event_ptr &event) override;

50

51bool cancel_order(const event_ptr &event) override;

52

53bool req_position() override;

54

55bool on_custom_event(const event_ptr &event) override;

56

57bool req_account() override;

58

59bool req_history_order(const event_ptr &event) override;

60

61bool req_history_trade(const event_ptr &event) override;

62

63void on_recover() override;

64

65/// 当客户端的某个连接与交易后台通信连接断开时,该方法被调用。

66///@param reason 错误原因,请与错误代码表对应

67///@param session_id 资金账户对应的session_id,登录时得到

68///@remark

69/// 用户主动调用logout导致的断线,不会触发此函数。api不会自动重连,当断线发生时,请用户自行选择后续操作,可以在此函数中调用Login重新登录,并更新session_id,此时用户收到的数据跟断线之前是连续的

70void OnDisconnected(uint64_t session_id, int reason) override;

71

72/// 错误应答

73///@param error_info

74/// 当服务器响应发生错误时的具体的错误代码和错误信息,当error_info为空,或者error_info.error_id为0时,表明没有错误

75///@remark 此函数只有在服务器发生错误时才会调用,一般无需用户处理

76void OnError(XTPRI *error_info) override{};

77

78/// 报单通知

79///@param order_info 订单响应具体信息,用户可以通过order_info.order_xtp_id来管理订单,通过GetClientIDByXTPID() ==

80/// client_id来过滤自己的订单,order_info.qty_left字段在订单为未成交、部成、全成、废单状态时,表示此订单还没有成交的数量,在部撤、全撤状态时,表示此订单被撤的数量。order_info.order_cancel_xtp_id为其所对应的撤单ID,不为0时表示此单被撤成功

81///@param error_info

82/// 订单被拒绝或者发生错误时错误代码和错误信息,当error_info为空,或者error_info.error_id为0时,表明没有错误

83///@remark

84/// 每次订单状态更新时,都会被调用,需要快速返回,否则会堵塞后续消息,当堵塞严重时,会触发断线,在订单未成交、全部成交、全部撤单、部分撤单、已拒绝这些状态时会有响应,对于部分成交的情况,请由订单的成交回报来自行确认。所有登录了此用户的客户端都将收到此用户的订单响应

85void OnOrderEvent(XTPOrderInfo *order_info, XTPRI *error_info, uint64_t session_id) override;

86

87/// 成交通知

88///@param trade_info 成交回报的具体信息,用户可以通过trade_info.order_xtp_id来管理订单,通过GetClientIDByXTPID() ==

89/// client_id来过滤自己的订单。对于上交所,exec_id可以唯一标识一笔成交。当发现2笔成交回报拥有相同的exec_id,则可以认为此笔交易自成交了。对于深交所,exec_id是唯一的,暂时无此判断机制。report_index+market字段可以组成唯一标识表示成交回报。

90///@remark

91/// 订单有成交发生的时候,会被调用,需要快速返回,否则会堵塞后续消息,当堵塞严重时,会触发断线。所有登录了此用户的客户端都将收到此用户的成交回报。相关订单为部成状态,需要用户通过成交回报的成交数量来确定,OnOrderEvent()不会推送部成状态。

92void OnTradeEvent(XTPTradeReport *trade_info, uint64_t session_id) override;

93

94/// 撤单出错响应

95///@param cancel_info 撤单具体信息,包括撤单的order_cancel_xtp_id和待撤单的order_xtp_id

96///@param error_info

97/// 撤单被拒绝或者发生错误时错误代码和错误信息,需要快速返回,否则会堵塞后续消息,当堵塞严重时,会触发断线,当error_info为空,或者error_info.error_id为0时,表明没有错误

98///@remark 此响应只会在撤单发生错误时被回调

99void OnCancelOrderError(XTPOrderCancelInfo *cancel_info, XTPRI *error_info, uint64_t session_id) override;

100

101/// 请求查询报单响应

102///@param order_info 查询到的一个报单

103///@param error_info

104/// 查询报单时发生错误时,返回的错误信息,当error_info为空,或者error_info.error_id为0时,表明没有错误

105///@param request_id 此消息响应函数对应的请求ID

106///@param is_last

107/// 此消息响应函数是否为request_id这条请求所对应的最后一个响应,当为最后一个的时候为true,如果为false,表示还有其他后续消息响应

108///@remark

109/// 由于支持分时段查询,一个查询请求可能对应多个响应,需要快速返回,否则会堵塞后续消息,当堵塞严重时,会触发断线

110void OnQueryOrder(XTPQueryOrderRsp *order_info, XTPRI *error_info, int request_id, bool is_last,

111 uint64_t session_id) override;

112

113/// 请求查询成交响应

114///@param trade_info 查询到的一个成交回报

115///@param error_info

116/// 查询成交回报发生错误时返回的错误信息,当error_info为空,或者error_info.error_id为0时,表明没有错误

117///@param request_id 此消息响应函数对应的请求ID

118///@param is_last

119/// 此消息响应函数是否为request_id这条请求所对应的最后一个响应,当为最后一个的时候为true,如果为false,表示还有其他后续消息响应

120///@remark

121/// 由于支持分时段查询,一个查询请求可能对应多个响应,需要快速返回,否则会堵塞后续消息,当堵塞严重时,会触发断线

122void OnQueryTrade(XTPQueryTradeRsp *trade_info, XTPRI *error_info, int request_id, bool is_last,

123 uint64_t session_id) override;

124

125/// 请求查询投资者持仓响应

126///@param position 查询到的一只股票的持仓情况

127///@param error_info

128/// 查询账户持仓发生错误时返回的错误信息,当error_info为空,或者error_info.error_id为0时,表明没有错误

129///@param request_id 此消息响应函数对应的请求ID

130///@param is_last

131/// 此消息响应函数是否为request_id这条请求所对应的最后一个响应,当为最后一个的时候为true,如果为false,表示还有其他后续消息响应

132///@remark

133/// 由于用户可能持有多个股票,一个查询请求可能对应多个响应,需要快速返回,否则会堵塞后续消息,当堵塞严重时,会触发断线

134void OnQueryPosition(XTPQueryStkPositionRsp *position, XTPRI *error_info, int request_id, bool is_last,

135 uint64_t session_id) override;

136

137/// 请求查询资金账户响应,需要快速返回,否则会堵塞后续消息,当堵塞严重时,会触发断线

138///@param asset 查询到的资金账户情况

139///@param error_info

140/// 查询资金账户发生错误时返回的错误信息,当error_info为空,或者error_info.error_id为0时,表明没有错误

141///@param request_id 此消息响应函数对应的请求ID

142///@param is_last

143/// 此消息响应函数是否为request_id这条请求所对应的最后一个响应,当为最后一个的时候为true,如果为false,表示还有其他后续消息响应

144///@remark 需要快速返回,否则会堵塞后续消息,当堵塞严重时,会触发断线

145void OnQueryAsset(XTPQueryAssetRsp *asset, XTPRI *error_info, int request_id, bool is_last,

146 uint64_t session_id) override;

147

148/// 请求查询分级基金信息响应,需要快速返回,否则会堵塞后续消息,当堵塞严重时,会触发断线

149///@param fund_info 查询到的分级基金情况

150///@param error_info

151/// 查询分级基金发生错误时返回的错误信息,当error_info为空,或者error_info.error_id为0时,表明没有错误

152///@param request_id 此消息响应函数对应的请求ID

153///@param is_last

154/// 此消息响应函数是否为request_id这条请求所对应的最后一个响应,当为最后一个的时候为true,如果为false,表示还有其他后续消息响应

155///@remark 需要快速返回,否则会堵塞后续消息,当堵塞严重时,会触发断线

156void OnQueryStructuredFund(XTPStructuredFundInfo *fund_info, XTPRI *error_info, int request_id, bool is_last,

157 uint64_t session_id) override{};

158

159/// 请求查询资金划拨订单响应,需要快速返回,否则会堵塞后续消息,当堵塞严重时,会触发断线

160///@param fund_transfer_info 查询到的资金账户情况

161///@param error_info

162/// 查询资金账户发生错误时返回的错误信息,当error_info为空,或者error_info.error_id为0时,表明没有错误

163///@param request_id 此消息响应函数对应的请求ID

164///@param is_last

165/// 此消息响应函数是否为request_id这条请求所对应的最后一个响应,当为最后一个的时候为true,如果为false,表示还有其他后续消息响应

166///@remark 需要快速返回,否则会堵塞后续消息,当堵塞严重时,会触发断线

167void OnQueryFundTransfer(XTPFundTransferNotice *fund_transfer_info, XTPRI *error_info, int request_id, bool is_last,

168 uint64_t session_id) override{};

169

170/// 资金划拨通知

171///@param fund_transfer_info

172/// 资金划拨通知的具体信息,用户可以通过fund_transfer_info.serial_id来管理订单,通过GetClientIDByXTPID() ==

173/// client_id来过滤自己的订单。

174///@param error_info

175/// 资金划拨订单被拒绝或者发生错误时错误代码和错误信息,当error_info为空,或者error_info.error_id为0时,表明没有错误

176///@remark

177/// 当资金划拨订单有状态变化的时候,会被调用,需要快速返回,否则会堵塞后续消息,当堵塞严重时,会触发断线。所有登录了此用户的客户端都将收到此用户的资金划拨通知。

178void OnFundTransfer(XTPFundTransferNotice *fund_transfer_info, XTPRI *error_info, uint64_t session_id) override{};

179

180/// 请求查询ETF清单文件的响应,需要快速返回,否则会堵塞后续消息,当堵塞严重时,会触发断线

181///@param etf_info 查询到的ETF清单文件情况

182///@param error_info

183/// 查询ETF清单文件发生错误时返回的错误信息,当error_info为空,或者error_info.error_id为0时,表明没有错误

184///@param request_id 此消息响应函数对应的请求ID

185///@param is_last

186/// 此消息响应函数是否为request_id这条请求所对应的最后一个响应,当为最后一个的时候为true,如果为false,表示还有其他后续消息响应

187///@remark 需要快速返回,否则会堵塞后续消息,当堵塞严重时,会触发断线

188void OnQueryETF(XTPQueryETFBaseRsp *etf_info, XTPRI *error_info, int request_id, bool is_last,

189 uint64_t session_id) override{};

190

191/// 请求查询ETF股票篮的响应,需要快速返回,否则会堵塞后续消息,当堵塞严重时,会触发断线

192///@param etf_component_info 查询到的ETF合约的相关成分股信息

193///@param error_info

194/// 查询ETF股票篮发生错误时返回的错误信息,当error_info为空,或者error_info.error_id为0时,表明没有错误

195///@param request_id 此消息响应函数对应的请求ID

196///@param is_last

197/// 此消息响应函数是否为request_id这条请求所对应的最后一个响应,当为最后一个的时候为true,如果为false,表示还有其他后续消息响应

198///@remark 需要快速返回,否则会堵塞后续消息,当堵塞严重时,会触发断线

199void OnQueryETFBasket(XTPQueryETFComponentRsp *etf_component_info, XTPRI *error_info, int request_id, bool is_last,

200 uint64_t session_id) override{};

201

202/// 请求查询今日新股申购信息列表的响应,需要快速返回,否则会堵塞后续消息,当堵塞严重时,会触发断线

203///@param ipo_info 查询到的今日新股申购的一只股票信息

204///@param error_info

205/// 查询今日新股申购信息列表发生错误时返回的错误信息,当error_info为空,或者error_info.error_id为0时,表明没有错误

206///@param request_id 此消息响应函数对应的请求ID

207///@param is_last

208/// 此消息响应函数是否为request_id这条请求所对应的最后一个响应,当为最后一个的时候为true,如果为false,表示还有其他后续消息响应

209///@remark 需要快速返回,否则会堵塞后续消息,当堵塞严重时,会触发断线

210void OnQueryIPOInfoList(XTPQueryIPOTickerRsp *ipo_info, XTPRI *error_info, int request_id, bool is_last,

211 uint64_t session_id) override{};

212

213/// 请求查询用户新股申购额度信息的响应,需要快速返回,否则会堵塞后续消息,当堵塞严重时,会触发断线

214///@param quota_info 查询到的用户某个市场的今日新股申购额度信息

215///@param error_info

216/// 查查询用户新股申购额度信息发生错误时返回的错误信息,当error_info为空,或者error_info.error_id为0时,表明没有错误

217///@param request_id 此消息响应函数对应的请求ID

218///@param is_last

219/// 此消息响应函数是否为request_id这条请求所对应的最后一个响应,当为最后一个的时候为true,如果为false,表示还有其他后续消息响应

220///@remark 需要快速返回,否则会堵塞后续消息,当堵塞严重时,会触发断线

221void OnQueryIPOQuotaInfo(XTPQueryIPOQuotaRsp *quota_info, XTPRI *error_info, int request_id, bool is_last,

222 uint64_t session_id) override{};

223

224private:

225TDConfiguration config_{};

226XTP::API::TraderApi *api_{};

227uint64_t session_id_{};

228int request_id_{};

229int get_request_id() { return ++request_id_; }

230std::string trading_day_{};

231

232std::unordered_map<uint64_t, uint64_t> map_kf_to_xtp_order_id_{};

233std::unordered_map<uint64_t, uint64_t> map_xtp_to_kf_order_id_{};

234std::unordered_map<uint64_t, uint64_t> map_request_location_{};

235std::unordered_map<uint64_t, std::unordered_set<std::string>> map_xtp_order_id_to_xtp_trader_ids_{};

236std::unordered_map<uint64_t, std::vector<XTPTradeReport>> map_xtp_order_id_to_XTPTradeReports_{};

237std::unordered_map<uint64_t, int64_t> map_xtp_order_id_to_traded_volume_{};

238std::unordered_map<uint64_t, std::queue<uint64_t>> map_xtp_order_id_to_action_ids_{};

239

240yijinjing::journal::writer_ptr get_history_writer(uint64_t request_id);

241

242bool custom_OnCancelOrderError(const event_ptr &event);

243bool custom_OnOrderEvent(const event_ptr &event);

244bool custom_OnTradeEvent(const event_ptr &event);

245bool custom_OnQueryOrder(const event_ptr &event);

246bool custom_OnQueryTrade(const event_ptr &event);

247bool custom_OnQueryAsset(const event_ptr &event);

248bool custom_OnQueryPosition(const event_ptr &event);

249

250bool custom_OnCancelOrderError(const XTPOrderCancelInfo &cancel_info, const XTPRI &error_info, uint64_t session_id);

251bool custom_OnOrderEvent(const XTPOrderInfo &order_info, const XTPRI &error_info, uint64_t session_id);

252bool custom_OnTradeEvent(const XTPTradeReport &trade_info, uint64_t session_id);

253bool custom_OnQueryOrder(const XTPOrderInfo &order_info, const XTPRI &error_info, int request_id, bool is_last,

254 uint64_t session_id);

255bool custom_OnQueryTrade(const XTPTradeReport &trade_info, const XTPRI &error_info, int request_id, bool is_last,

256 uint64_t session_id);

257bool custom_OnQueryAsset(const XTPQueryAssetRsp &asset, const XTPRI &error_info, int request_id, bool is_last,

258 uint64_t session_id);

259bool custom_OnQueryPosition(const XTPQueryStkPositionRsp &position, const XTPRI &error_info, int request_id,

260 bool is_last, uint64_t session_id);

261

262void try_deal_XTPTradeReport(uint64_t xtp_order_id);

263bool generate_external_order(const XTPOrderInfo &order_info);

264

265void add_XTPTradeReport(const XTPTradeReport &trade_info);

266bool has_dealt_trade(uint64_t xtp_order_id, const std::string &exec_id);

267void add_dealt_trade(uint64_t xtp_order_id, const std::string &exec_id);

268

269void add_traded_volume(uint64_t order_xtp_id, int64_t trade_volume);

270int64_t get_traded_volume(uint64_t order_xtp_id);

271

272void add_action_id(uint64_t xtp_order_id, int64_t action_id);

273uint64_t get_action_id(uint64_t xtp_order_id);

274

275void req_order_trade();

276void try_ready();

277bool req_order_over_{false};

278bool req_trade_over_{false};

279};

280} // namespace kungfu::wingchun::xtp

281#endif // KUNGFU_XTP_EXT_TRADER_H

trader_xtp.cpp文件

xtp的交易柜台函数实现

1#include "trader_xtp.h"

2#include "buffer_data.h"

3#include "serialize_xtp.h"

4#include "type_convert.h"

5#include <algorithm>

6

7namespace kungfu::wingchun::xtp {

8using namespace kungfu::yijinjing::data;

9using namespace kungfu::yijinjing;

10

11TraderXTP::TraderXTP(broker::BrokerVendor &vendor) : Trader(vendor) {

12 KUNGFU_SETUP_LOG();

13 SPDLOG_DEBUG("arguments: {}", get_vendor().get_arguments());

14}

15

16TraderXTP::~TraderXTP() {

17 if (api_ != nullptr) {

18 api_->Release();

19 }

20}

21

22void TraderXTP::pre_start() {

23 config_ = nlohmann::json::parse(get_config());

24 SPDLOG_INFO("config: {}", get_config());

25 if (not config_.recover_order_trade) {

26 disable_recover();

27 }

28}

29

30void TraderXTP::on_start() {

31 if (config_.client_id < 1 or config_.client_id > 99) {

32 SPDLOG_ERROR("client_id must between 1 and 99");

33 }

34 std::string runtime_folder = get_runtime_folder();

35 SPDLOG_INFO("Connecting XTP account {} with tcp://{}:{}", config_.account_id, config_.td_ip, config_.td_port);

36 api_ = XTP::API::TraderApi::CreateTraderApi(config_.client_id, runtime_folder.c_str());

37 api_->RegisterSpi(this);

38 api_->SubscribePublicTopic(XTP_TERT_QUICK);

39 api_->SetSoftwareVersion("1.1.0");

40 api_->SetSoftwareKey(config_.software_key.c_str());

41 session_id_ = api_->Login(config_.td_ip.c_str(), config_.td_port, config_.account_id.c_str(),

42 config_.password.c_str(), XTP_PROTOCOL_TCP);

43 if (session_id_ > 0) {

44 SPDLOG_INFO("Login successfully");

45 req_order_trade();

46 } else {

47 update_broker_state(BrokerState::LoginFailed);

48 SPDLOG_ERROR("Login failed [{}]: {}", api_->GetApiLastError()->error_id, api_->GetApiLastError()->error_msg);

49 }

50}

51

52void TraderXTP::on_exit() {

53 if (api_ != nullptr and session_id_ > 0) {

54 auto result = api_->Logout(session_id_);

55 SPDLOG_INFO("Logout with return code {}", result);

56 }

57}

58

59bool TraderXTP::insert_order(const event_ptr &event) {

60 const OrderInput &input = event->data<OrderInput>();

61 SPDLOG_DEBUG("OrderInput: {}", input.to_string());

62 XTPOrderInsertInfo xtp_input = {};

63 to_xtp(xtp_input, input);

64

65 SPDLOG_DEBUG("XTPOrderInsertInfo: {}", to_string(xtp_input));

66 uint64_t order_xtp_id = api_->InsertOrder(&xtp_input, session_id_);

67 auto success = order_xtp_id != 0;

68

69 auto nano = yijinjing::time::now_in_nano();

70 auto writer = get_writer(event->source());

71 Order &order = writer->open_data<Order>(event->gen_time());

72 order_from_input(input, order);

73 order.external_order_id = std::to_string(order_xtp_id).c_str();

74 order.insert_time = nano;

75 order.update_time = nano;

76

77 if (success) {

78 map_kf_to_xtp_order_id_.emplace(uint64_t(input.order_id), order_xtp_id);

79 map_xtp_to_kf_order_id_.emplace(order_xtp_id, uint64_t(input.order_id));

80 } else {

81 auto error_info = api_->GetApiLastError();

82 order.error_id = error_info->error_id;

83 order.error_msg = error_info->error_msg;

84 order.status = OrderStatus::Error;

85 }

86

87 SPDLOG_DEBUG("Order: {}", order.to_string());

88 writer->close_data();

89 if (not success) {

90 SPDLOG_ERROR("fail to insert order {}, error id {}, {}", to_string(xtp_input), (int)order.error_id,

91 order.error_msg);

92 }

93 return success;

94}

95

96bool TraderXTP::cancel_order(const event_ptr &event) {

97 const OrderAction &action = event->data<OrderAction>();

98 SPDLOG_DEBUG("OrderAction: {}", action.to_string());

99 auto order_id_iter = map_kf_to_xtp_order_id_.find(action.order_id);

100 if (order_id_iter == map_kf_to_xtp_order_id_.end()) {

101 SPDLOG_ERROR("failed to cancel order {}, can't find related xtp order id", action.order_id);

102 return false;

103 }

104

105 if (not has_order(action.order_id)) {

106 SPDLOG_ERROR("no order_id {} in orders_", action.order_id);

107 return false;

108 }

109

110 auto &order_state = get_order(action.order_id);

111 uint64_t order_xtp_id = order_id_iter->second;

112 add_action_id(order_xtp_id, action.order_action_id);

113 auto xtp_action_id = api_->CancelOrder(order_xtp_id, session_id_);

114 auto success = xtp_action_id != 0;

115

116 if (not success) {

117 XTPRI *error_info = api_->GetApiLastError();

118 SPDLOG_ERROR("failed to cancel order {}, order_xtp_id: {} session_id: {} error_id: {} error_msg: {}",

119 action.order_id, order_xtp_id, session_id_, error_info->error_id, error_info->error_msg);

120 OrderActionError &error = get_writer(event->source())->open_data<OrderActionError>(now());

121 error.order_id = action.order_id; // 订单ID

122 std::string str_external_order_id = std::to_string(order_xtp_id);

123 error.external_order_id = str_external_order_id.c_str();

124 error.order_action_id = action.order_action_id; // 订单操作ID,

125 error.error_id = xtp_action_id; // 错误ID

126 error.error_msg = error_info->error_msg; // 错误信息

127 error.insert_time = time::now_in_nano(); // 写入时间

128 SPDLOG_DEBUG("OrderActionError: {}", error.to_string());

129 get_writer(event->source())->close_data();

130 return false;

131 }

132

133 if (not is_final_status(order_state.data.status) or order_state.data.status == OrderStatus::Lost) {

134 order_state.data.status = OrderStatus::Cancelling;

135 try_write_to(order_state.data, order_state.dest);

136 }

137 SPDLOG_DEBUG("Order: {}", order_state.data.to_string());

138 return success;

139}

140

141bool TraderXTP::req_position() {

142 SPDLOG_INFO("req_position");

143 return api_->QueryPosition(nullptr, session_id_, get_request_id()) == 0;

144}

145

146bool TraderXTP::req_account() {

147 SPDLOG_INFO("req_account");

148 return api_->QueryAsset(session_id_, get_request_id()) == 0;

149}

150

151void TraderXTP::OnDisconnected(uint64_t session_id, int reason) {

152 if (session_id == session_id_) {

153 update_broker_state(BrokerState::DisConnected);

154 SPDLOG_ERROR("disconnected, reason: {}", reason);

155 }

156}

157

158void TraderXTP::OnOrderEvent(XTPOrderInfo *order_info, XTPRI *error_info, uint64_t session_id) {

159 if (nullptr == order_info) {

160 SPDLOG_ERROR("XTPOrderInfo is nullptr");

161 return;

162 }

163 SPDLOG_DEBUG("XTPOrderInfo: {}", to_string(*order_info));

164 auto &bf_order_info = get_thread_writer()->open_custom_data<BufferXTPOrderInfo>(kXTPOrderInfoType, now());

165 memcpy(&bf_order_info.order_info, order_info, sizeof(XTPOrderInfo));

166 bf_order_info.session_id = session_id;

167 if (error_info != nullptr) {

168 memcpy(&bf_order_info.error_info, error_info, sizeof(XTPRI));

169 } else {

170 memset(&bf_order_info.error_info, 0, sizeof(XTPRI));

171 }

172 SPDLOG_DEBUG("BufferXTPOrderInfo: {}", to_string(bf_order_info));

173 get_thread_writer()->close_data();

174}

175

176bool TraderXTP::custom_OnOrderEvent(const event_ptr &event) {

177 const auto *bf_order_info = reinterpret_cast<const BufferXTPOrderInfo *>(event->data_address());

178 return custom_OnOrderEvent(bf_order_info->order_info, bf_order_info->error_info, bf_order_info->session_id);

179}

180

181bool TraderXTP::custom_OnOrderEvent(const XTPOrderInfo &order_info, const XTPRI &error_info, uint64_t session_id) {

182 SPDLOG_DEBUG("XTPOrderInfo: {}", to_string(order_info));

183 SPDLOG_DEBUG("session_id: {}, XTPRI: {}", session_id, to_string(error_info));

184

185 auto order_xtp_id_iter = map_xtp_to_kf_order_id_.find(order_info.order_xtp_id);

186 if (order_xtp_id_iter == map_xtp_to_kf_order_id_.end()) {

187 SPDLOG_WARN("unrecognized order_xtp_id {}@{}", order_info.order_xtp_id, trading_day_);

188 return generate_external_order(order_info);

189 }

190

191 uint64_t kf_order_id = order_xtp_id_iter->second;

192 if (not has_order(kf_order_id)) {

193 return generate_external_order(order_info);

194 }

195

196 auto &order_state = get_order(kf_order_id);

197 if (not is_final_status(order_state.data.status) or order_state.data.status == OrderStatus::Lost) {

198 from_xtp_no_price_type(order_info, order_state.data);

199 order_state.data.update_time = yijinjing::time::now_in_nano();

200 if (error_info.error_id != 0) {

201 order_state.data.error_id = error_info.error_id;

202 order_state.data.error_msg = error_info.error_msg;

203 }

204 try_write_to(order_state.data, order_state.dest);

205 SPDLOG_DEBUG("Order: {}", order_state.data.to_string());

206 try_deal_XTPTradeReport(order_info.order_xtp_id);

207 }

208 return true;

209}

210

211bool TraderXTP::generate_external_order(const XTPOrderInfo &order_info) {

212 SPDLOG_DEBUG("XTPOrderInfo: {}", to_string(order_info));

213 static const std::unordered_set<int> set_cancel_enum = {

214 XTP_ORDER_SUBMIT_STATUS_TYPE::XTP_ORDER_SUBMIT_STATUS_CANCEL_SUBMITTED, //

215 XTP_ORDER_SUBMIT_STATUS_TYPE::XTP_ORDER_SUBMIT_STATUS_CANCEL_REJECTED, //

216 XTP_ORDER_SUBMIT_STATUS_TYPE::XTP_ORDER_SUBMIT_STATUS_CANCEL_ACCEPTED //

217 };

218

219 if (not config_.sync_external_order) {

220 return false;

221 }

222

223 if (set_cancel_enum.find(order_info.order_submit_status) != set_cancel_enum.end()) {

224 SPDLOG_DEBUG("this XTPOrderInfo is xtp cancel order, do not generate kungfu Order");

225 return false;

226 }

227

228 auto writer = get_public_writer();

229 auto nano = yijinjing::time::now_in_nano();

230 Order &order = writer->open_data<Order>(now());

231 order.order_id = writer->current_frame_uid();

232 from_xtp(order_info, order);

233 order.insert_time = nsec_from_xtp_timestamp(order_info.insert_time);

234 order.update_time = nano;

235 map_kf_to_xtp_order_id_.emplace(uint64_t(order.order_id), order_info.order_xtp_id);

236 map_xtp_to_kf_order_id_.emplace(order_info.order_xtp_id, uint64_t(order.order_id));

237 SPDLOG_DEBUG("Order: {}", order.to_string());

238 writer->close_data();

239 try_deal_XTPTradeReport(order_info.order_xtp_id);

240 return true;

241}

242

243void TraderXTP::OnTradeEvent(XTPTradeReport *trade_info, uint64_t session_id) {

244 if (nullptr == trade_info) {

245 SPDLOG_ERROR("XTPTradeReport is nullptr");

246 return;

247 }

248 SPDLOG_DEBUG("XTPTradeReport: {}", to_string(*trade_info));

249

250 auto &bf_trade_info = get_thread_writer()->open_custom_data<BufferXTPTradeReport>(kXTPTradeReportType, now());

251 memcpy(&bf_trade_info.trade_info, trade_info, sizeof(XTPTradeReport));

252 bf_trade_info.session_id = session_id;

253 SPDLOG_DEBUG("BufferXTPOrderInfo: {}", to_string(bf_trade_info));

254 get_thread_writer()->close_data();

255}

256

257bool TraderXTP::custom_OnTradeEvent(const XTPTradeReport &trade_info, uint64_t session_id) {

258 SPDLOG_DEBUG("XTPTradeReport: {}", to_string(trade_info));

259 SPDLOG_DEBUG("session_id: {}", session_id);

260

261 auto order_xtp_id_iter = map_xtp_to_kf_order_id_.find(trade_info.order_xtp_id);

262 if (order_xtp_id_iter == map_xtp_to_kf_order_id_.end()) {

263 SPDLOG_WARN("unrecognized order_xtp_id {}, store in map_xtp_order_id_to_XTPTradeReports_",

264 trade_info.order_xtp_id);

265 add_XTPTradeReport(trade_info);

266 return false;

267 }

268

269 if (has_dealt_trade(trade_info.order_xtp_id, trade_info.exec_id)) {

270 SPDLOG_DEBUG("order_xtp_id:{}, exec_id: {}, has dealt", trade_info.order_xtp_id, trade_info.exec_id);

271 return false;

272 }

273

274 uint64_t kf_order_id = order_xtp_id_iter->second;

275 if (not has_order(kf_order_id)) {

276 SPDLOG_ERROR("no order_id {} in orders_", kf_order_id);

277 return false;

278 }

279

280 add_dealt_trade(trade_info.order_xtp_id, trade_info.exec_id);

281 auto &order_state = get_order(kf_order_id);

282

283 if (has_writer(order_state.dest)) {

284 auto writer = get_writer(order_state.dest);

285 Trade &trade = writer->open_data<Trade>(now());

286 from_xtp(trade_info, trade);

287 trade.trade_id = writer->current_frame_uid();

288 trade.order_id = kf_order_id;

289 add_traded_volume(trade_info.order_xtp_id, trade.volume);

290 SPDLOG_DEBUG("Trade: {}", trade.to_string());

291 writer->close_data();

292 } else {

293 Trade trade{};

294 from_xtp(trade_info, trade);

295 trade.trade_id = get_public_writer()->current_frame_uid() xor (time::now_in_nano() & 0xFFFFFFFF);

296 trade.order_id = kf_order_id;

297 add_traded_volume(trade_info.order_xtp_id, trade.volume);

298 SPDLOG_DEBUG("Trade: {}", trade.to_string());

299 try_write_to(trade, order_state.dest);

300 }

301

302 if (not is_final_status(order_state.data.status) or order_state.data.status == OrderStatus::Lost) {

303 order_state.data.volume_left = std::min<int64_t>(

304 order_state.data.volume_left, order_state.data.volume - get_traded_volume(trade_info.order_xtp_id));